64 KiB

![]()

FreqAI

FreqAI is a module designed to automate a variety of tasks associated with training a predictive machine learning model to generate market forecasts given a set of input features.

Features include:

- Self-adaptive retraining: retrain models during live deployments to self-adapt to the market in an unsupervised manner.

- Rapid feature engineering: create large rich feature sets (10k+ features) based on simple user-created strategies.

- High performance: adaptive retraining occurs on a separate thread (or on GPU if available) from inferencing and bot trade operations. Newest models and data are kept in memory for rapid inferencing.

- Realistic backtesting: emulate self-adaptive retraining with a backtesting module that automates past retraining.

- Modifiability: use the generalized and robust architecture for incorporating any machine learning library/method available in Python. Eight examples are currently available, including classifiers, regressors, and a convolutional neural network.

- Smart outlier removal: remove outliers from training and prediction data sets using a variety of outlier detection techniques.

- Crash resilience: store model to disk to make reloading from a crash fast and easy, and purge obsolete files for sustained dry/live runs.

- Automatic data normalization: normalize the data in a smart and statistically safe way.

- Automatic data download: compute the data download timerange and update historic data (in live deployments).

- Cleaning of incoming data: handle NaNs safely before training and prediction.

- Dimensionality reduction: reduce the size of the training data via Principal Component Analysis.

- Deploying bot fleets: set one bot to train models while a fleet of follower bots inference the models and handle trades.

Quick start

The easiest way to quickly test FreqAI is to run it in dry mode with the following command

freqtrade trade --config config_examples/config_freqai.example.json --strategy FreqaiExampleStrategy --freqaimodel LightGBMRegressor --strategy-path freqtrade/templates

The user will see the boot-up process of automatic data downloading, followed by simultaneous training and trading.

The example strategy, example prediction model, and example config can be found in

freqtrade/templates/FreqaiExampleStrategy.py, freqtrade/freqai/prediction_models/LightGBMRegressor.py, and

config_examples/config_freqai.example.json, respectively.

General approach

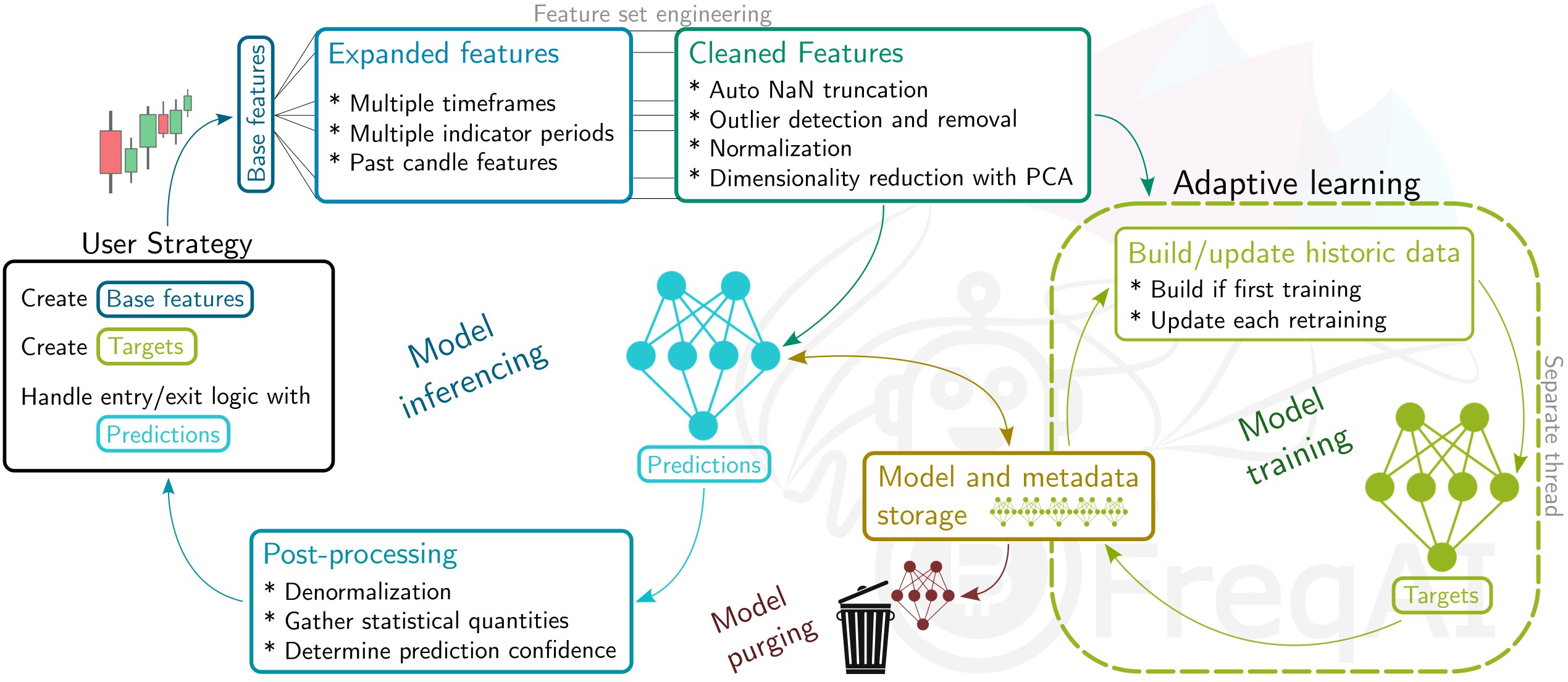

The user provides FreqAI with a set of custom base indicators (the same way as in a typical Freqtrade strategy) as well as target values (labels). FreqAI trains a model to predict the target values based on the input of custom indicators, for each pair in the whitelist. These models are consistently retrained to adapt to market conditions. FreqAI offers the ability to both backtest strategies (emulating reality with periodic retraining) and deploy dry/live runs. In dry/live conditions, FreqAI can be set to constant retraining in a background thread in an effort to keep models as up to date as possible.

An overview of the algorithm is shown below, explaining the data processing pipeline and the model usage.

Important machine learning vocabulary

Features - the quantities with which a model is trained. All features for a single candle is stored as a vector. In FreqAI, the user builds the feature sets from anything they can construct in the strategy.

Labels - the target values that a model is trained toward. Each set of features is associated with a single label that is defined by the user within the strategy. These labels intentionally look into the future, and are not available to the model during dry/live/backtesting.

Training - the process of feeding individual feature sets, composed of historic data, with associated labels into the model with the goal of matching input feature sets to associated labels.

Train data - a subset of the historic data that is fed to the model during training. This data directly influences weight connections in the model.

Test data - a subset of the historic data that is used to evaluate the performance of the model after training. This data does not influence nodal weights within the model.

Install prerequisites

The normal Freqtrade install process will ask the user if they wish to install FreqAI dependencies. The user should reply "yes" to this question if they wish to use FreqAI. If the user did not reply yes, they can manually install these dependencies after the install with:

pip install -r requirements-freqai.txt

!!! Note Catboost will not be installed on arm devices (raspberry, Mac M1, ARM based VPS, ...), since Catboost does not provide wheels for this platform.

Usage with docker

For docker users, a dedicated tag with freqAI dependencies is available as :freqai.

As such - you can replace the image line in your docker-compose file with image: freqtradeorg/freqtrade:develop_freqai.

This image contains the regular freqAI dependencies. Similar to native installs, Catboost will not be available on ARM based devices.

Setting up FreqAI

Parameter table

The table below will list all configuration parameters available for FreqAI, presented in the same order as config_examples/config_freqai.example.json.

Mandatory parameters are marked as Required, which means that they are required to be set in one of the possible ways.

| Parameter | Description |

|---|---|

| General configuration parameters | |

freqai |

Required. The parent dictionary containing all the parameters for controlling FreqAI. Datatype: Dictionary. |

purge_old_models |

Delete obsolete models (otherwise, all historic models will remain on disk). Datatype: Boolean. Default: False. |

train_period_days |

Required. Number of days to use for the training data (width of the sliding window). Datatype: Positive integer. |

backtest_period_days |

Required. Number of days to inference from the trained model before sliding the window defined above, and retraining the model. This can be fractional days, but beware that the user-provided timerange will be divided by this number to yield the number of trainings necessary to complete the backtest. Datatype: Float. |

save_backtest_models |

Backtesting operates most efficiently by saving the prediction data and reusing them directly for subsequent runs (when users wish to tune entry/exit parameters). If a user wishes to save models to disk when running backtesting, they should activate save_backtest_models. A user may wish to do this if they plan to use the same model files for starting a dry/live instance with the same identifier. Datatype: Boolean. Default: False. |

identifier |

Required. A unique name for the current model. This can be reused to reload pre-trained models/data. Datatype: String. |

live_retrain_hours |

Frequency of retraining during dry/live runs. Default set to 0, which means the model will retrain as often as possible. Datatype: Float > 0. |

expiration_hours |

Avoid making predictions if a model is more than expiration_hours old. Defaults set to 0, which means models never expire. Datatype: Positive integer. |

fit_live_predictions_candles |

Number of historical candles to use for computing target (label) statistics from prediction data, instead of from the training data set. Datatype: Positive integer. |

follow_mode |

If true, this instance of FreqAI will look for models associated with identifier and load those for inferencing. A follower will not train new models. Datatype: Boolean. Default: False. |

continual_learning |

If true, FreqAI will start training new models from the final state of the most recently trained model. Datatype: Boolean. Default: False. |

| Feature parameters | |

feature_parameters |

A dictionary containing the parameters used to engineer the feature set. Details and examples are shown here. Datatype: Dictionary. |

include_timeframes |

A list of timeframes that all indicators in populate_any_indicators will be created for. The list is added as features to the base asset feature set. Datatype: List of timeframes (strings). |

include_corr_pairlist |

A list of correlated coins that FreqAI will add as additional features to all pair_whitelist coins. All indicators set in populate_any_indicators during feature engineering (see details here) will be created for each coin in this list, and that set of features is added to the base asset feature set. Datatype: List of assets (strings). |

label_period_candles |

Number of candles into the future that the labels are created for. This is used in populate_any_indicators (see templates/FreqaiExampleStrategy.py for detailed usage). The user can create custom labels, making use of this parameter or not. Datatype: Positive integer. |

include_shifted_candles |

Add features from previous candles to subsequent candles to add historical information. FreqAI takes all features from the include_shifted_candles previous candles, duplicates and shifts them so that the information is available for the subsequent candle. Datatype: Positive integer. |

weight_factor |

Used to set weights for training data points according to their recency. See details about how it works here. Datatype: Positive float (typically < 1). |

indicator_max_period_candles |

No longer used. User must use the strategy set startup_candle_count which defines the maximum period used in populate_any_indicators() for indicator creation (timeframe independent). FreqAI uses this information in combination with the maximum timeframe to calculate how many data points it should download so that the first data point does not have a NaN Datatype: positive integer. |

indicator_periods_candles |

Calculate indicators for indicator_periods_candles time periods and add them to the feature set. Datatype: List of positive integers. |

stratify_training_data |

This value is used to indicate the grouping of the data. For example, 2 would set every 2nd data point into a separate dataset to be pulled from during training/testing. See details about how it works here Datatype: Positive integer. |

principal_component_analysis |

Automatically reduce the dimensionality of the data set using Principal Component Analysis. See details about how it works here |

plot_feature_importance |

Create an interactive feature importance plot for each model. Datatype: Boolean. Datatype: Boolean, defaults to False |

DI_threshold |

Activates the Dissimilarity Index for outlier detection when > 0. See details about how it works here. Datatype: Positive float (typically < 1). |

use_SVM_to_remove_outliers |

Train a support vector machine to detect and remove outliers from the training data set, as well as from incoming data points. See details about how it works here. Datatype: Boolean. |

svm_params |

All parameters available in Sklearn's SGDOneClassSVM(). See details about some select parameters here. Datatype: Dictionary. |

use_DBSCAN_to_remove_outliers |

Cluster data using DBSCAN to identify and remove outliers from training and prediction data. See details about how it works here. Datatype: Boolean. |

inlier_metric_window |

If set, FreqAI will add the inlier_metric to the training feature set and set the lookback to be the inlier_metric_window. Details of how the inlier_metric is computed can be found here Datatype: int. Default: 0 |

noise_standard_deviation |

If > 0, FreqAI adds noise to the training features. FreqAI generates random deviates from a gaussian distribution with a standard deviation of noise_standard_deviation and adds them to all data points. Value should be kept relative to the normalized space between -1 and 1). In other words, since data is always normalized between -1 and 1 in FreqAI, the user can expect a noise_standard_deviation: 0.05 to see 32% of data randomly increased/decreased by more than 2.5% (i.e. the percent of data falling within the first standard deviation). Good for preventing overfitting. Datatype: int. Default: 0 |

outlier_protection_percentage |

If more than outlier_protection_percentage % of points are detected as outliers by the SVM or DBSCAN, FreqAI will log a warning message and ignore outlier detection while keeping the original dataset intact. If the outlier protection is triggered, no predictions will be made based on the training data. Datatype: Float. Default: 30 |

reverse_train_test_order |

If true, FreqAI will train on the latest data split and test on historical split of the data. This allows the model to be trained up to the most recent data point, while avoiding overfitting. However, users should be careful to understand unorthodox nature of this parameter before employing it. Datatype: Boolean. Default: False |

| Data split parameters | |

data_split_parameters |

Include any additional parameters available from Scikit-learn test_train_split(), which are shown here (external website). Datatype: Dictionary. |

test_size |

Fraction of data that should be used for testing instead of training. Datatype: Positive float < 1. |

shuffle |

Shuffle the training data points during training. Typically, for time-series forecasting, this is set to False. Datatype: Boolean. |

| Model training parameters | |

model_training_parameters |

A flexible dictionary that includes all parameters available by the user selected model library. For example, if the user uses LightGBMRegressor, this dictionary can contain any parameter available by the LightGBMRegressor here (external website). If the user selects a different model, such as PPO from stable_baselines3, this dictionary can contain any parameter from that model. Datatype: Dictionary. |

n_estimators |

The number of boosted trees to fit in regression. Datatype: Integer. |

learning_rate |

Boosting learning rate during regression. Datatype: Float. |

n_jobs, thread_count, task_type |

Set the number of threads for parallel processing and the task_type (gpu or cpu). Different model libraries use different parameter names. Datatype: Float. |

| Reinforcement Learning Parameters* | |

rl_config |

A dictionary containing the control parameters for a Reinforcement Learning model. Datatype: Dictionary. |

train_cycles |

Training time steps will be set based on the `train_cycles * number of training data points. Datatype: Integer. |

thread_count |

Number of threads to dedicate to the Reinforcement Learning training process. Datatype: int. |

max_trade_duration_candles |

Guides the agent training to keep trades below desired length. Example usage shown in prediction_models/ReinforcementLearner.py within the user customizable calculate_reward() Datatype: int. |

model_type |

Model string from stable_baselines3 or SBcontrib. Available strings include: 'TRPO', 'ARS', 'RecurrentPPO', 'MaskablePPO', 'PPO', 'A2C', 'DQN'. User should ensure that model_training_parameters match those available to the corresponding stable_baselines3 model by visiting their documentaiton. PPO doc (external website) Datatype: string. |

policy_type |

One of the available policy types from stable_baselines3 Datatype: string. |

continual_learning |

If true, the agent will start new trainings from the model selected during the previous training. If false, a new agent is trained from scratch for each training. Datatype: Bool. |

thread_count |

Number of threads to dedicate to the Reinforcement Learning training process. Datatype: int. |

model_reward_parameters |

Parameters used inside the user customizable calculate_reward() function in ReinforcementLearner.py Datatype: int. |

| Extraneous parameters | |

keras |

If your model makes use of keras (typical of Tensorflow based prediction models), activate this flag so that the model save/loading follows keras standards. Default value false Datatype: boolean. |

conv_width |

The width of a convolutional neural network input tensor or the ReinforcementLearningModel window_size. This replaces the need for shift by feeding in historical data points as the second dimension of the tensor. Technically, this parameter can also be used for regressors, but it only adds computational overhead and does not change the model training/prediction. Default value, 2 Datatype: integer. |

Important dataframe key patterns

Below are the values the user can expect to include/use inside a typical strategy dataframe (df[]):

| DataFrame Key | Description |

|---|---|

df['&*'] |

Any dataframe column prepended with & in populate_any_indicators() is treated as a training target (label) inside FreqAI (typically following the naming convention &-s*). The names of these dataframe columns are fed back to the user as the predictions. For example, if the user wishes to predict the price change in the next 40 candles (similar to templates/FreqaiExampleStrategy.py), they set df['&-s_close']. FreqAI makes the predictions and gives them back under the same key (df['&-s_close']) to be used in populate_entry/exit_trend(). Datatype: Depends on the output of the model. |

df['&*_std/mean'] |

Standard deviation and mean values of the user-defined labels during training (or live tracking with fit_live_predictions_candles). Commonly used to understand the rarity of a prediction (use the z-score as shown in templates/FreqaiExampleStrategy.py to evaluate how often a particular prediction was observed during training or historically with fit_live_predictions_candles). Datatype: Float. |

df['do_predict'] |

Indication of an outlier data point. The return value is integer between -1 and 2, which lets the user know if the prediction is trustworthy or not. do_predict==1 means the prediction is trustworthy. If the Dissimilarity Index (DI, see details here) of the input data point is above the user-defined threshold, FreqAI will subtract 1 from do_predict, resulting in do_predict==0. If use_SVM_to_remove_outliers() is active, the Support Vector Machine (SVM) may also detect outliers in training and prediction data. In this case, the SVM will also subtract 1 from do_predict. If the input data point was considered an outlier by the SVM but not by the DI, the result will be do_predict==0. If both the DI and the SVM considers the input data point to be an outlier, the result will be do_predict==-1. A particular case is when do_predict == 2, which means that the model has expired due to exceeding expired_hours. Datatype: Integer between -1 and 2. |

df['DI_values'] |

Dissimilarity Index values are proxies to the level of confidence FreqAI has in the prediction. A lower DI means the prediction is close to the training data, i.e., higher prediction confidence. Datatype: Float. |

df['%*'] |

Any dataframe column prepended with % in populate_any_indicators() is treated as a training feature. For example, the user can include the RSI in the training feature set (similar to in templates/FreqaiExampleStrategy.py) by setting df['%-rsi']. See more details on how this is done here. Note: Since the number of features prepended with % can multiply very quickly (10s of thousands of features is easily engineered using the multiplictative functionality described in the feature_parameters table shown above), these features are removed from the dataframe upon return from FreqAI. If the user wishes to keep a particular type of feature for plotting purposes, they can prepend it with %%. Datatype: Depends on the output of the model. |

File structure

user_data_dir/models/ contains all the data associated with the trainings and backtests.

This file structure is heavily controlled and inferenced by the FreqaiDataKitchen()

and should therefore not be modified.

Example config file

The user interface is isolated to the typical Freqtrade config file. A FreqAI config should include:

"freqai": {

"enabled": true,

"startup_candles": 10000,

"purge_old_models": true,

"train_period_days": 30,

"backtest_period_days": 7,

"identifier" : "unique-id",

"feature_parameters" : {

"include_timeframes": ["5m","15m","4h"],

"include_corr_pairlist": [

"ETH/USD",

"LINK/USD",

"BNB/USD"

],

"label_period_candles": 24,

"include_shifted_candles": 2,

"indicator_periods_candles": [10, 20]

},

"data_split_parameters" : {

"test_size": 0.25

},

"model_training_parameters" : {

"n_estimators": 100

},

}

Building a FreqAI strategy

The FreqAI strategy requires the user to include the following lines of code in the standard Freqtrade strategy:

# user should define the maximum startup candle count (the largest number of candles

# passed to any single indicator)

startup_candle_count: int = 20

def populate_indicators(self, dataframe: DataFrame, metadata: dict) -> DataFrame:

# the model will return all labels created by user in `populate_any_indicators`

# (& appended targets), an indication of whether or not the prediction should be accepted,

# the target mean/std values for each of the labels created by user in

# `populate_any_indicators()` for each training period.

dataframe = self.freqai.start(dataframe, metadata, self)

return dataframe

def populate_any_indicators(

self, pair, df, tf, informative=None, set_generalized_indicators=False

):

"""

Function designed to automatically generate, name and merge features

from user indicated timeframes in the configuration file. User controls the indicators

passed to the training/prediction by prepending indicators with `'%-' + coin `

(see convention below). I.e. user should not prepend any supporting metrics

(e.g. bb_lowerband below) with % unless they explicitly want to pass that metric to the

model.

:param pair: pair to be used as informative

:param df: strategy dataframe which will receive merges from informatives

:param tf: timeframe of the dataframe which will modify the feature names

:param informative: the dataframe associated with the informative pair

:param coin: the name of the coin which will modify the feature names.

"""

coin = pair.split('/')[0]

if informative is None:

informative = self.dp.get_pair_dataframe(pair, tf)

# first loop is automatically duplicating indicators for time periods

for t in self.freqai_info["feature_parameters"]["indicator_periods_candles"]:

t = int(t)

informative[f"%-{coin}rsi-period_{t}"] = ta.RSI(informative, timeperiod=t)

informative[f"%-{coin}mfi-period_{t}"] = ta.MFI(informative, timeperiod=t)

informative[f"%-{coin}adx-period_{t}"] = ta.ADX(informative, window=t)

indicators = [col for col in informative if col.startswith("%")]

# This loop duplicates and shifts all indicators to add a sense of recency to data

for n in range(self.freqai_info["feature_parameters"]["include_shifted_candles"] + 1):

if n == 0:

continue

informative_shift = informative[indicators].shift(n)

informative_shift = informative_shift.add_suffix("_shift-" + str(n))

informative = pd.concat((informative, informative_shift), axis=1)

df = merge_informative_pair(df, informative, self.config["timeframe"], tf, ffill=True)

skip_columns = [

(s + "_" + tf) for s in ["date", "open", "high", "low", "close", "volume"]

]

df = df.drop(columns=skip_columns)

# Add generalized indicators here (because in live, it will call this

# function to populate indicators during training). Notice how we ensure not to

# add them multiple times

if set_generalized_indicators:

# user adds targets here by prepending them with &- (see convention below)

# If user wishes to use multiple targets, a multioutput prediction model

# needs to be used such as templates/CatboostPredictionMultiModel.py

df["&-s_close"] = (

df["close"]

.shift(-self.freqai_info["feature_parameters"]["label_period_candles"])

.rolling(self.freqai_info["feature_parameters"]["label_period_candles"])

.mean()

/ df["close"]

- 1

)

return df

Notice how the populate_any_indicators() is where the user adds their own features (more information) and labels (more information). See a full example at templates/FreqaiExampleStrategy.py.

Important: The self.freqai.start() function cannot be called outside the populate_indicators().

Setting the startup_candle_count

Users need to take care to set the startup_candle_count in their strategy the same way they would for any normal Freqtrade strategy (see details here). This value is used by Freqtrade to ensure that a sufficient amount of data is provided when calling on the dataprovider to avoid any NaNs at the beginning of the first training. Users can easily set this value by identifying the longest period (in candle units) that they pass to their indicator creation functions (e.g. talib functions). In the present example, the user would pass 20 to as this value (since it is the maximum value in their indicators_periods_candles).

!!! Note

Typically it is best for users to be safe and multiply their expected startup_candle_count by 2. There are instances where the talib functions actually require more data than just the passed period. Anecdotally, multiplying the startup_candle_count by 2 always leads to a fully NaN free training dataset. Look out for this log message to confirm that your data is clean:

```

2022-08-31 15:14:04 - freqtrade.freqai.data_kitchen - INFO - dropped 0 training points due to NaNs in populated dataset 4319.

```

Creating a dynamic target

The &*_std/mean return values describe the statistical fit of the user defined label during the most recent training. This value allows the user to know the rarity of a given prediction. For example, templates/FreqaiExampleStrategy.py, creates a target_roi which is based on filtering out predictions that are below a given z-score of 1.25.

dataframe["target_roi"] = dataframe["&-s_close_mean"] + dataframe["&-s_close_std"] * 1.25

dataframe["sell_roi"] = dataframe["&-s_close_mean"] - dataframe["&-s_close_std"] * 1.25

If the user wishes to consider the population

of historical predictions for creating the dynamic target instead of the trained labels, (as discussed above) the user

can do so by setting fit_live_prediction_candles in the config to the number of historical prediction candles

the user wishes to use to generate target statistics.

"freqai": {

"fit_live_prediction_candles": 300,

}

If the user sets this value, FreqAI will initially use the predictions from the training data

and subsequently begin introducing real prediction data as it is generated. FreqAI will save

this historical data to be reloaded if the user stops and restarts a model with the same identifier.

Building a custom prediction model

FreqAI has multiple example prediction model libraries, such as Catboost regression (freqai/prediction_models/CatboostRegressor.py) and LightGBM regression.

However, the user can customize and create their own prediction models using the IFreqaiModel class.

The user is encouraged to inherit train() and predict() to let them customize various aspects of their training procedures.

Feature engineering

Features are added by the user inside the populate_any_indicators() method of the strategy

by prepending indicators with %, and labels with &.

There are some important components/structures that the user must include when building their feature set; the use of these is shown below:

def populate_any_indicators(

self, pair, df, tf, informative=None, set_generalized_indicators=False

):

"""

Function designed to automatically generate, name, and merge features

from user-indicated timeframes in the configuration file. The user controls the indicators

passed to the training/prediction by prepending indicators with `'%-' + coin `

(see convention below). I.e., the user should not prepend any supporting metrics

(e.g., bb_lowerband below) with % unless they explicitly want to pass that metric to the

model.

:param pair: pair to be used as informative

:param df: strategy dataframe which will receive merges from informatives

:param tf: timeframe of the dataframe which will modify the feature names

:param informative: the dataframe associated with the informative pair

:param coin: the name of the coin which will modify the feature names.

"""

coin = pair.split('/')[0]

if informative is None:

informative = self.dp.get_pair_dataframe(pair, tf)

# first loop is automatically duplicating indicators for time periods

for t in self.freqai_info["feature_parameters"]["indicator_periods_candles"]:

t = int(t)

informative[f"%-{coin}rsi-period_{t}"] = ta.RSI(informative, timeperiod=t)

informative[f"%-{coin}mfi-period_{t}"] = ta.MFI(informative, timeperiod=t)

informative[f"%-{coin}adx-period_{t}"] = ta.ADX(informative, window=t)

bollinger = qtpylib.bollinger_bands(

qtpylib.typical_price(informative), window=t, stds=2.2

)

informative[f"{coin}bb_lowerband-period_{t}"] = bollinger["lower"]

informative[f"{coin}bb_middleband-period_{t}"] = bollinger["mid"]

informative[f"{coin}bb_upperband-period_{t}"] = bollinger["upper"]

informative[f"%-{coin}bb_width-period_{t}"] = (

informative[f"{coin}bb_upperband-period_{t}"]

- informative[f"{coin}bb_lowerband-period_{t}"]

) / informative[f"{coin}bb_middleband-period_{t}"]

informative[f"%-{coin}close-bb_lower-period_{t}"] = (

informative["close"] / informative[f"{coin}bb_lowerband-period_{t}"]

)

informative[f"%-{coin}relative_volume-period_{t}"] = (

informative["volume"] / informative["volume"].rolling(t).mean()

)

indicators = [col for col in informative if col.startswith("%")]

# This loop duplicates and shifts all indicators to add a sense of recency to data

for n in range(self.freqai_info["feature_parameters"]["include_shifted_candles"] + 1):

if n == 0:

continue

informative_shift = informative[indicators].shift(n)

informative_shift = informative_shift.add_suffix("_shift-" + str(n))

informative = pd.concat((informative, informative_shift), axis=1)

df = merge_informative_pair(df, informative, self.config["timeframe"], tf, ffill=True)

skip_columns = [

(s + "_" + tf) for s in ["date", "open", "high", "low", "close", "volume"]

]

df = df.drop(columns=skip_columns)

# Add generalized indicators here (because in live, it will call this

# function to populate indicators during training). Notice how we ensure not to

# add them multiple times

if set_generalized_indicators:

df["%-day_of_week"] = (df["date"].dt.dayofweek + 1) / 7

df["%-hour_of_day"] = (df["date"].dt.hour + 1) / 25

# user adds targets here by prepending them with &- (see convention below)

# If user wishes to use multiple targets, a multioutput prediction model

# needs to be used such as templates/CatboostPredictionMultiModel.py

df["&-s_close"] = (

df["close"]

.shift(-self.freqai_info["feature_parameters"]["label_period_candles"])

.rolling(self.freqai_info["feature_parameters"]["label_period_candles"])

.mean()

/ df["close"]

- 1

)

return df

In the presented example strategy, the user does not wish to pass the bb_lowerband as a feature to the model,

and has therefore not prepended it with %. The user does, however, wish to pass bb_width to the

model for training/prediction and has therefore prepended it with %.

The include_timeframes in the example config above are the timeframes (tf) of each call to populate_any_indicators() in the strategy. In the present case, the user is asking for the

5m, 15m, and 4h timeframes of the rsi, mfi, roc, and bb_width to be included in the feature set.

The user can ask for each of the defined features to be included also from

informative pairs using the include_corr_pairlist. This means that the feature

set will include all the features from populate_any_indicators on all the include_timeframes for each of the correlated pairs defined in the config (ETH/USD, LINK/USD, and BNB/USD).

include_shifted_candles indicates the number of previous

candles to include in the feature set. For example, include_shifted_candles: 2 tells

FreqAI to include the past 2 candles for each of the features in the feature set.

In total, the number of features the user of the presented example strat has created is:

length of include_timeframes * no. features in populate_any_indicators() * length of include_corr_pairlist * no. include_shifted_candles * length of indicator_periods_candles

= 3 * 3 * 3 * 2 * 2 = 108.

Another structure to consider is the location of the labels at the bottom of the example function (below if set_generalized_indicators:).

This is where the user will add single features and labels to their feature set to avoid duplication of them from

various configuration parameters that multiply the feature set, such as include_timeframes.

!!! Note

Features must be defined in populate_any_indicators(). Definining FreqAI features in populate_indicators()

will cause the algorithm to fail in live/dry mode. If the user wishes to add generalized features that are not associated with

a specific pair or timeframe, they should use the following structure inside populate_any_indicators()

(as exemplified in freqtrade/templates/FreqaiExampleStrategy.py):

```python

def populate_any_indicators(self, metadata, pair, df, tf, informative=None, coin="", set_generalized_indicators=False):

...

# Add generalized indicators here (because in live, it will call only this function to populate

# indicators for retraining). Notice how we ensure not to add them multiple times by associating

# these generalized indicators to the basepair/timeframe

if set_generalized_indicators:

df['%-day_of_week'] = (df["date"].dt.dayofweek + 1) / 7

df['%-hour_of_day'] = (df['date'].dt.hour + 1) / 25

# user adds targets here by prepending them with &- (see convention below)

# If user wishes to use multiple targets, a multioutput prediction model

# needs to be used such as templates/CatboostPredictionMultiModel.py

df["&-s_close"] = (

df["close"]

.shift(-self.freqai_info["feature_parameters"]["label_period_candles"])

.rolling(self.freqai_info["feature_parameters"]["label_period_candles"])

.mean()

/ df["close"]

- 1

)

```

(Please see the example script located in `freqtrade/templates/FreqaiExampleStrategy.py` for a full example of `populate_any_indicators()`.)

Setting classifier targets

FreqAI includes the CatboostClassifier via the flag --freqaimodel CatboostClassifier. The user should take care to set the classes using strings:

df['&s-up_or_down'] = np.where( df["close"].shift(-100) > df["close"], 'up', 'down')

Additionally, the example classifier models do not accommodate multiple labels, but they do allow multi-class classification within a single label column.

Running FreqAI

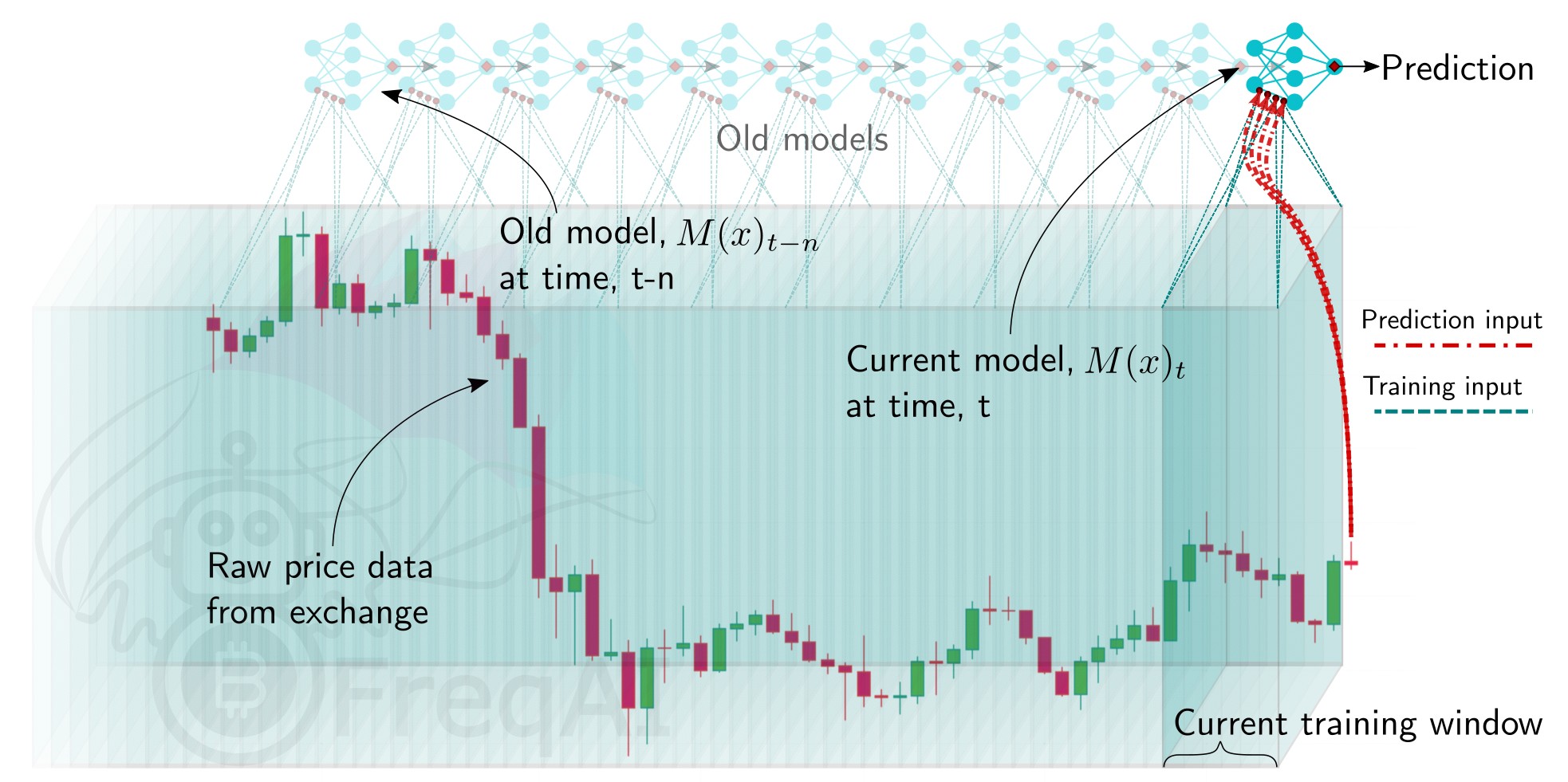

There are two ways to train and deploy an adaptive machine learning model. FreqAI enables live deployment as well as backtesting analyses. In both cases, a model is trained periodically, as shown in the following figure.

Running the model live

FreqAI can be run dry/live using the following command:

freqtrade trade --strategy FreqaiExampleStrategy --config config_freqai.example.json --freqaimodel LightGBMRegressor

By default, FreqAI will not find any existing models and will start by training a new one

based on the user's configuration settings. Following training, the model will be used to make predictions on incoming candles until a new model is available. New models are typically generated as often as possible, with FreqAI managing an internal queue of the coin pairs to try to keep all models equally up to date. FreqAI will always use the most recently trained model to make predictions on incoming live data. If the user does not want FreqAI to retrain new models as often as possible, they can set live_retrain_hours to tell FreqAI to wait at least that number of hours before training a new model. Additionally, the user can set expired_hours to tell FreqAI to avoid making predictions on models that are older than that number of hours.

If the user wishes to start a dry/live run from a saved backtest model (or from a previously crashed dry/live session), the user only needs to reuse

the same identifier parameter:

"freqai": {

"identifier": "example",

"live_retrain_hours": 0.5

}

In this case, although FreqAI will initiate with a

pre-trained model, it will still check to see how much time has elapsed since the model was trained,

and if a full live_retrain_hours has elapsed since the end of the loaded model, FreqAI will retrain.

Backtesting

The FreqAI backtesting module can be executed with the following command:

freqtrade backtesting --strategy FreqaiExampleStrategy --strategy-path freqtrade/templates --config config_examples/config_freqai.example.json --freqaimodel LightGBMRegressor --timerange 20210501-20210701

Backtesting mode requires the user to have the data pre-downloaded (unlike in dry/live mode where FreqAI automatically downloads the necessary data). The user should be careful to consider that the time range of the downloaded data is more than the backtesting time range. This is because FreqAI needs data prior to the desired backtesting time range in order to train a model to be ready to make predictions on the first candle of the user-set backtesting time range. More details on how to calculate the data to download can be found here.

If this command has never been executed with the existing config file, it will train a new model

for each pair, for each backtesting window within the expanded --timerange.

!!! Note "Model reuse"

Once the training is completed, the user can execute the backtesting again with the same config file and

FreqAI will find the trained models and load them instead of spending time training. This is useful

if the user wants to tweak (or even hyperopt) buy and sell criteria inside the strategy. If the user

wants to retrain a new model with the same config file, then they should simply change the identifier.

This way, the user can return to using any model they wish by simply specifying the identifier.

Hyperopt

Users can hyperopt using the same command as typical hyperopt:

freqtrade hyperopt --hyperopt-loss SharpeHyperOptLoss --strategy FreqaiExampleStrategy --freqaimodel LightGBMRegressor --strategy-path freqtrade/templates --config config_examples/config_freqai.example.json --timerange 20220428-20220507

Users need to have the data pre-downloaded in the same fashion as if they were doing a FreqAI backtest. In addition, users must consider some restrictions when trying to Hyperopt FreqAI strategies:

- The

--analyze-per-epochhyperopt parameter is not compatible with FreqAI. - It's not possible to hyperopt indicators in

populate_any_indicators()function. This means that the user cannot optimize model parameters using hyperopt. Apart from this exception, it is possible to optimize all other spaces. - The Backtesting instructions also apply to Hyperopt.

The best method for combining hyperopt and FreqAI is to focus on hyperopting entry/exit thresholds/criteria. Users need to focus on hyperopting parameters that are not used in their FreqAI features. For example, users should not try to hyperopt rolling window lengths in their feature creation, or any of their FreqAI config which changes predictions. In order to efficiently hyperopt the FreqAI strategy, FreqAI stores predictions as dataframes and reuses them. Hence the requirement to hyperopt entry/exit thresholds/criteria only.

A good example of a hyperoptable parameter in FreqAI is a value for DI_values beyond which we consider outliers and below which we consider inliers:

di_max = IntParameter(low=1, high=20, default=10, space='buy', optimize=True, load=True)

dataframe['outlier'] = np.where(dataframe['DI_values'] > self.di_max.value/10, 1, 0)

Which would help the user understand the appropriate Dissimilarity Index values for their particular parameter space.

Deciding the size of the sliding training window and backtesting duration

The user defines the backtesting timerange with the typical --timerange parameter in the

configuration file. The duration of the sliding training window is set by train_period_days, whilst

backtest_period_days is the sliding backtesting window, both in number of days (backtest_period_days can be

a float to indicate sub-daily retraining in live/dry mode). In the presented example config,

the user is asking FreqAI to use a training period of 30 days and backtest on the subsequent 7 days.

This means that if the user sets --timerange 20210501-20210701,

FreqAI will train have trained 8 separate models at the end of --timerange (because the full range comprises 8 weeks). After the training of the model, FreqAI will backtest the subsequent 7 days. The "sliding window" then moves one week forward (emulating FreqAI retraining once per week in live mode) and the new model uses the previous 30 days (including the 7 days used for backtesting by the previous model) to train. This is repeated until the end of --timerange.

!!! Note

Although fractional backtest_period_days is allowed, the user should be aware that the --timerange is divided by this value to determine the number of models that FreqAI will need to train in order to backtest the full range. For example, if the user wants to set a --timerange of 10 days, and asks for a backtest_period_days of 0.1, FreqAI will need to train 100 models per pair to complete the full backtest. Because of this, a true backtest of FreqAI adaptive training would take a very long time. The best way to fully test a model is to run it dry and let it constantly train. In this case, backtesting would take the exact same amount of time as a dry run.

Downloading data for backtesting

Live/dry instances will download the data automatically for the user, but users who wish to use backtesting functionality still need to download the necessary data using download-data (details here). FreqAI users need to pay careful attention to understanding how much additional data needs to be downloaded to ensure that they have a sufficient amount of training data before the start of their backtesting timerange. The amount of additional data can be roughly estimated by moving the start date of the timerange backwards by train_period_days and the startup_candle_count (details) from the beginning of the desired backtesting timerange.

As an example, if we wish to backtest the --timerange above of 20210501-20210701, and we use the example config which sets train_period_days to 15. The startup candle count is 40 on a maximum include_timeframes of 1h. We would need 20210501 - 15 days - 40 * 1h / 24 hours = 20210414 (16.7 days earlier than the start of the desired training timerange).

Defining model expirations

During dry/live mode, FreqAI trains each coin pair sequentially (on separate threads/GPU from the main Freqtrade bot). This means that there is always an age discrepancy between models. If a user is training on 50 pairs, and each pair requires 5 minutes to train, the oldest model will be over 4 hours old. This may be undesirable if the characteristic time scale (the trade duration target) for a strategy is less than 4 hours. The user can decide to only make trade entries if the model is less than

a certain number of hours old by setting the expiration_hours in the config file:

"freqai": {

"expiration_hours": 0.5,

}

In the presented example config, the user will only allow predictions on models that are less than 1/2 hours old.

Purging old model data

FreqAI stores new model files each time it retrains. These files become obsolete as new models are trained and FreqAI adapts to new market conditions. Users planning to leave FreqAI running for extended periods of time with high frequency retraining should enable purge_old_models in their config:

"freqai": {

"purge_old_models": true,

}

This will automatically purge all models older than the two most recently trained ones.

Returning additional info from training

The user may find that there are some important metrics that they'd like to return to the strategy at the end of each model training.

The user can include these metrics by assigning them to dk.data['extra_returns_per_train']['my_new_value'] = XYZ inside their custom prediction model class. FreqAI takes the my_new_value assigned in this dictionary and expands it to fit the return dataframe to the strategy.

The user can then use the value in the strategy with dataframe['my_new_value']. An example of how this is already used in FreqAI is

the &*_mean and &*_std values, which indicate the mean and standard deviation of the particular target (label) during the most recent training.

An example, where the user wants to use live metrics from the trade database, is shown below:

"freqai": {

"extra_returns_per_train": {"total_profit": 4}

}

The user needs to set the standard dictionary in the config so that FreqAI can return proper dataframe shapes. These values will likely be overridden by the prediction model, but in the case where the model has yet to set them, or needs a default initial value, this is the value that will be returned.

Setting up a follower

The user can define:

"freqai": {

"follow_mode": true,

"identifier": "example"

}

to indicate to the bot that it should not train models, but instead should look for models trained by a leader with the same identifier. In this example, the user has a leader bot with the identifier: "example". The leader bot is already running or launching simultaneously as the follower.

The follower will load models created by the leader and inference them to obtain predictions.

Data manipulation techniques

Feature normalization

The feature set created by the user is automatically normalized to the training data. This includes all test data and unseen prediction data (dry/live/backtest).

Reducing data dimensionality with Principal Component Analysis

Users can reduce the dimensionality of their features by activating the principal_component_analysis in the config:

"freqai": {

"feature_parameters" : {

"principal_component_analysis": true

}

}

This will perform PCA on the features and reduce the dimensionality of the data so that the explained variance of the data set is >= 0.999.

Stratifying the data for training and testing the model

The user can stratify (group) the training/testing data using:

"freqai": {

"feature_parameters" : {

"stratify_training_data": 3

}

}

This will split the data chronologically so that every Xth data point is used to test the model after training. In the example above, the user is asking for every third data point in the dataframe to be used for testing; the other points are used for training.

The test data is used to evaluate the performance of the model after training. If the test score is high, the model is able to capture the behavior of the data well. If the test score is low, either the model either does not capture the complexity of the data, the test data is significantly different from the train data, or a different model should be used.

Using the inlier_metric

The inlier_metric is a metric aimed at quantifying how different a prediction data point is from the most recent historic data points.

User can set inlier_metric_window to set the look back window. FreqAI will compute the distance between the present prediction point and each of the previous data points (total of inlier_metric_window points).

This function goes one step further - during training, it computes the inlier_metric for all training data points and builds weibull distributions for each each lookback point. The cumulative distribution function for the weibull distribution is used to produce a quantile for each of the data points. The quantiles for each lookback point are averaged to create the inlier_metric.

FreqAI adds this inlier_metric score to the training features! In other words, your model is trained to recognize how this temporal inlier metric is related to the user set labels.

This function does not remove outliers from the data set.

Controlling the model learning process

Model training parameters are unique to the machine learning library selected by the user. FreqAI allows the user to set any parameter for any library using the model_training_parameters dictionary in the user configuration file. The example configuration file (found in config_examples/config_freqai.example.json) show some of the example parameters associated with Catboost and LightGBM, but the user can add any parameters available in those libraries.

Data split parameters are defined in data_split_parameters which can be any parameters associated with Sklearn's train_test_split() function.

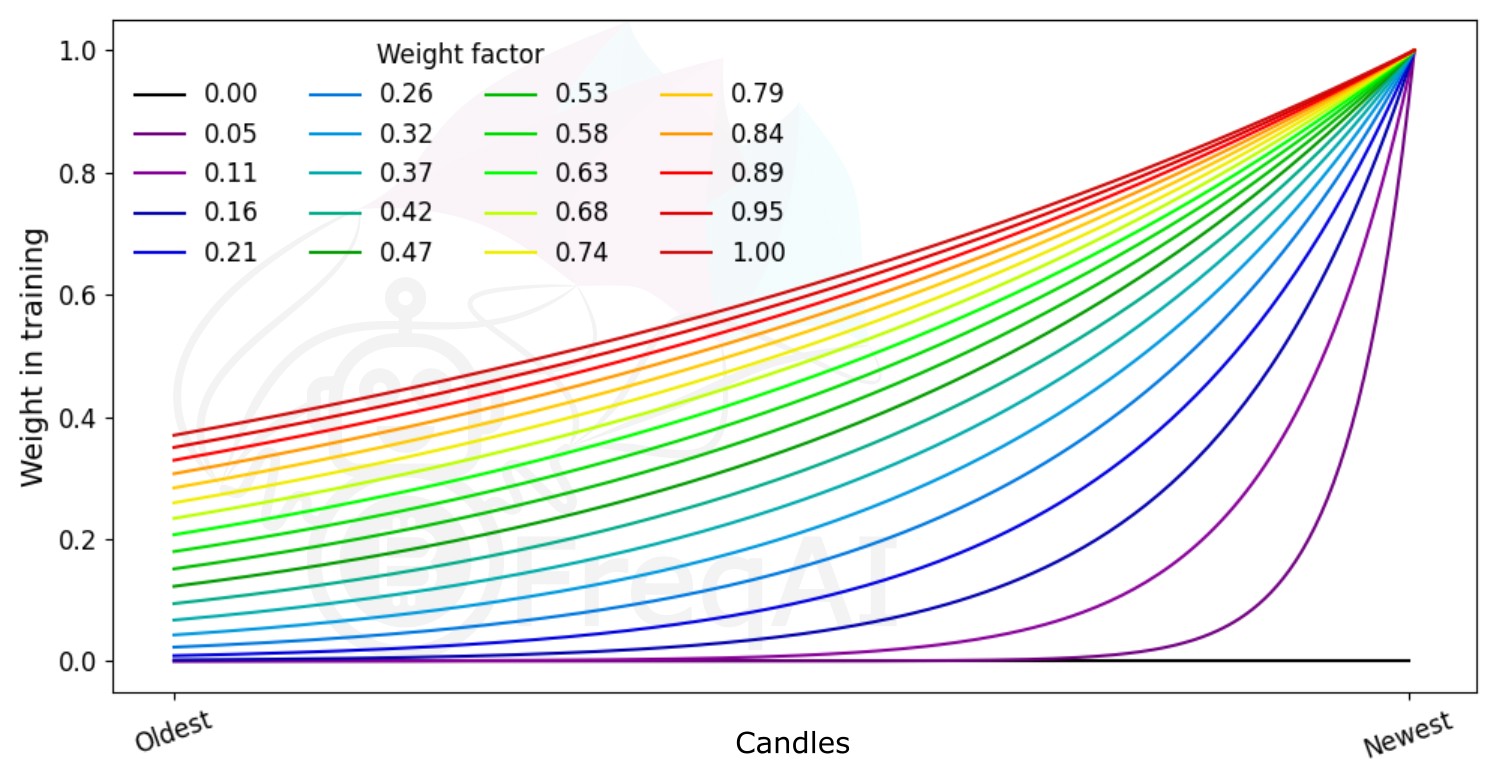

FreqAI includes some additional parameters such as weight_factor, which allows the user to weight more recent data more strongly

than past data via an exponential function:

W_i = \exp(\frac{-i}{\alpha*n}) where W_i is the weight of data point i in a total set of n data points. Below is a figure showing the effect of different weight factors on the data points (candles) in a feature set.

train_test_split() has a parameters called shuffle that allows the user to keep the data unshuffled. This is particularly useful to avoid biasing training with temporally auto-correlated data.

Finally, label_period_candles defines the offset (number of candles into the future) used for the labels. In the presented example config,

the user is asking for labels that are 24 candles in the future.

Outlier removal

Removing outliers with the Dissimilarity Index

The user can tell FreqAI to remove outlier data points from the training/test data sets using a Dissimilarity Index by including the following statement in the config:

"freqai": {

"feature_parameters" : {

"DI_threshold": 1

}

}

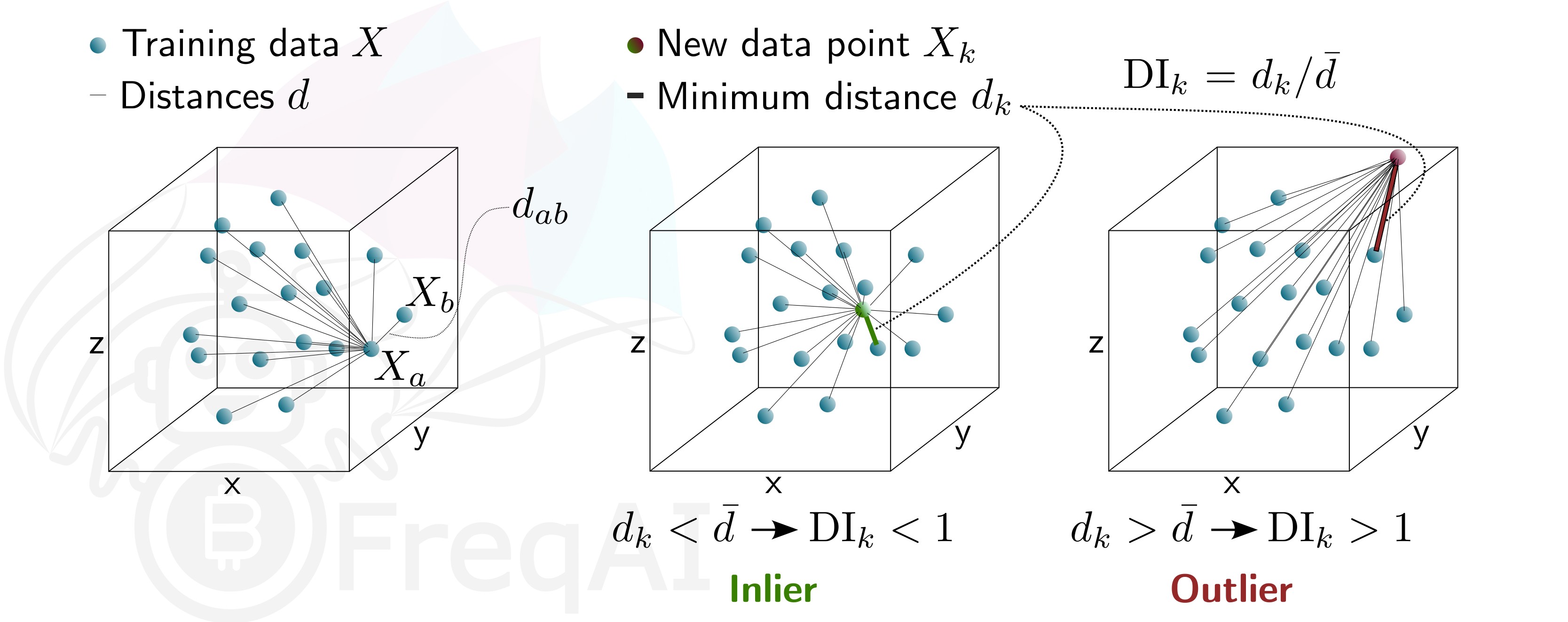

Equity and crypto markets suffer from a high level of non-patterned noise in the form of outlier data points. The Dissimilarity Index (DI) aims to quantify the uncertainty associated with each prediction made by the model. The DI allows predictions which are outliers (not existent in the model feature space) to be thrown out due to low levels of certainty.

To do so, FreqAI measures the distance between each training data point (feature vector), X_{a}, and all other training data points:

d_{ab} = \sqrt{\sum_{j=1}^p(X_{a,j}-X_{b,j})^2} where d_{ab} is the distance between the normalized points a and b. p is the number of features, i.e., the length of the vector X. The characteristic distance, \overline{d} for a set of training data points is simply the mean of the average distances:

\overline{d} = \sum_{a=1}^n(\sum_{b=1}^n(d_{ab}/n)/n) \overline{d} quantifies the spread of the training data, which is compared to the distance between a new prediction feature vectors, X_k and all the training data:

d_k = \arg \min d_{k,i} which enables the estimation of the Dissimilarity Index as:

DI_k = d_k/\overline{d} The user can tweak the DI through the DI_threshold to increase or decrease the extrapolation of the trained model.

Below is a figure that describes the DI for a 3D data set.

Removing outliers using a Support Vector Machine (SVM)

The user can tell FreqAI to remove outlier data points from the training/test data sets using a SVM by setting:

"freqai": {

"feature_parameters" : {

"use_SVM_to_remove_outliers": true

}

}

FreqAI will train an SVM on the training data (or components of it if the user activated

principal_component_analysis) and remove any data point that the SVM deems to be beyond the feature space.

The parameter shuffle is by default set to False to ensure consistent results. If it is set to True, running the SVM multiple times on the same data set might result in different outcomes due to max_iter being to low for the algorithm to reach the demanded tol. Increasing max_iter solves this issue but causes the procedure to take longer time.

The parameter nu, very broadly, is the amount of data points that should be considered outliers.

Removing outliers with DBSCAN

The user can configure FreqAI to use DBSCAN to cluster and remove outliers from the training/test data set or incoming outliers from predictions, by activating use_DBSCAN_to_remove_outliers in the config:

"freqai": {

"feature_parameters" : {

"use_DBSCAN_to_remove_outliers": true

}

}

DBSCAN is an unsupervised machine learning algorithm that clusters data without needing to know how many clusters there should be.

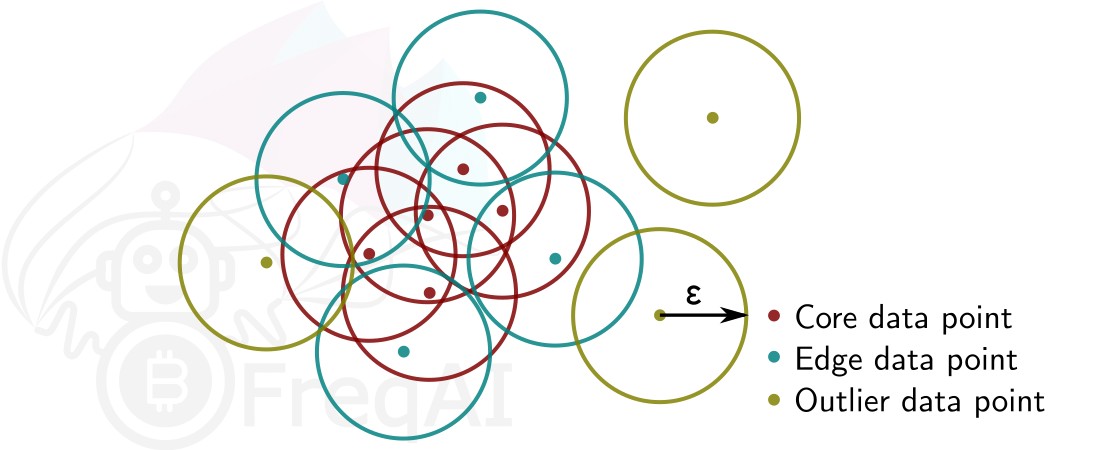

Given a number of data points N, and a distance \varepsilon, DBSCAN clusters the data set by setting all data points that have N-1 other data points within a distance of \varepsilon as core points. A data point that is within a distance of \varepsilon from a core point but that does not have N-1 other data points within a distance of \varepsilon from itself is considered an edge point. A cluster is then the collection of core points and edge points. Data points that have no other data points at a distance <\varepsilon are considered outliers. The figure below shows a cluster with N = 3.

FreqAI uses sklearn.cluster.DBSCAN (details are available on scikit-learn's webpage here) with min_samples (N) taken as double the no. of user-defined features, and eps (\varepsilon) taken as the longest distance in the k-distance graph computed from the nearest neighbors in the pairwise distances of all data points in the feature set.

Additional information

Common pitfalls

FreqAI cannot be combined with dynamic VolumePairlists (or any pairlist filter that adds and removes pairs dynamically).

This is for performance reasons - FreqAI relies on making quick predictions/retrains. To do this effectively,

it needs to download all the training data at the beginning of a dry/live instance. FreqAI stores and appends

new candles automatically for future retrains. This means that if new pairs arrive later in the dry run due to a volume pairlist, it will not have the data ready. However, FreqAI does work with the ShuffleFilter or a VolumePairlist which keeps the total pairlist constant (but reorders the pairs according to volume).

Credits

FreqAI was developed by a group of individuals who all contributed specific skillsets to the project.

Conception and software development: Robert Caulk @robcaulk

Theoretical brainstorming, data analysis: Elin Törnquist @th0rntwig

Code review, software architecture brainstorming: @xmatthias

Beta testing and bug reporting: @bloodhunter4rc, Salah Lamkadem @ikonx, @ken11o2, @longyu, @paranoidandy, @smidelis, @smarm, Juha Nykänen @suikula, Wagner Costa @wagnercosta

Reinforcement Learning

Setting up and running a Reinforcement Learning model is as quick and simple as running a Regressor. Users can start training and trading live from example files using:

freqtrade trade --freqaimodel ReinforcementLearner --strategy ReinforcementLearningExample5ac --strategy-path freqtrade/freqai/example_strats --config config_examples/config_freqai-rl.example.json

As users begin to modify the strategy and the prediction model, they will quickly realize some important differences between the Reinforcement Learner and the Regressors/Classifiers. Firstly, the strategy does not set a target value (no labels!). Instead, the user sets a calculate_reward() function inside their custom ReinforcementLearner.py file. A default calculate_reward() is provided inside prediction_models/ReinforcementLearner.py to give users the necessary building blocks to start their own models. It is inside the calculate_reward() where users express their creative theories about the market. For example, the user wants to reward their agent when it makes a winning trade, and penalize the agent when it makes a losing trade. Or perhaps, the user wishes to reward the agnet for entering trades, and penalize the agent for sitting in trades too long. Below we show examples of how these rewards are all calculated:

class MyRLEnv(Base5ActionRLEnv):

"""

User made custom environment. This class inherits from BaseEnvironment and gym.env.

Users can override any functions from those parent classes. Here is an example

of a user customized `calculate_reward()` function.

"""

def calculate_reward(self, action):

# first, penalize if the action is not valid

if not self._is_valid(action):

return -2

pnl = self.get_unrealized_profit()

rew = np.sign(pnl) * (pnl + 1)

factor = 100

# reward agent for entering trades

if action in (Actions.Long_enter.value, Actions.Short_enter.value) \

and self._position == Positions.Neutral:

return 25

# discourage agent from not entering trades

if action == Actions.Neutral.value and self._position == Positions.Neutral:

return -1

max_trade_duration = self.rl_config.get('max_trade_duration_candles', 300)

trade_duration = self._current_tick - self._last_trade_tick

if trade_duration <= max_trade_duration:

factor *= 1.5

elif trade_duration > max_trade_duration:

factor *= 0.5

# discourage sitting in position

if self._position in (Positions.Short, Positions.Long) and \

action == Actions.Neutral.value:

return -1 * trade_duration / max_trade_duration

# close long

if action == Actions.Long_exit.value and self._position == Positions.Long:

if pnl > self.profit_aim * self.rr:

factor *= self.rl_config['model_reward_parameters'].get('win_reward_factor', 2)

return float(rew * factor)

# close short

if action == Actions.Short_exit.value and self._position == Positions.Short:

if pnl > self.profit_aim * self.rr:

factor *= self.rl_config['model_reward_parameters'].get('win_reward_factor', 2)

return float(rew * factor)

return 0.

After users realize there are no labels to set, they will soon understand that the agent is making its "own" entry and exit decisions. This makes strategy construction rather simple. The entry and exit signals come from the agent in the form of an integer - which are used directly to decide entries and exits in the strategy:

def populate_any_indicators(

self, pair, df, tf, informative=None, set_generalized_indicators=False

):

...

if set_generalized_indicators:

# For RL, there are no direct targets to set. This sets the base action to neutral

# until the agent sends an action.

df["&-action"] = 0

return df

and then the &-action will be used in populate_entry/exit functions:

def populate_entry_trend(self, df: DataFrame, metadata: dict) -> DataFrame:

enter_long_conditions = [df["do_predict"] == 1, df["&-action"] == 1]

if enter_long_conditions:

df.loc[

reduce(lambda x, y: x & y, enter_long_conditions), ["enter_long", "enter_tag"]

] = (1, "long")

enter_short_conditions = [df["do_predict"] == 1, df["&-action"] == 3]

if enter_short_conditions:

df.loc[

reduce(lambda x, y: x & y, enter_short_conditions), ["enter_short", "enter_tag"]

] = (1, "short")

return df

def populate_exit_trend(self, df: DataFrame, metadata: dict) -> DataFrame:

exit_long_conditions = [df["do_predict"] == 1, df["&-action"] == 2]

if exit_long_conditions:

df.loc[reduce(lambda x, y: x & y, exit_long_conditions), "exit_long"] = 1

exit_short_conditions = [df["do_predict"] == 1, df["&-action"] == 4]

if exit_short_conditions:

df.loc[reduce(lambda x, y: x & y, exit_short_conditions), "exit_short"] = 1

return df

Users should be careful to consider that &-action depends on which environment they choose to use. The example above shows 5 actions, where 0 is neutral, 1 is enter long, 2 is exit long, 3 is enter short and 4 is exit short.

Using Tensorboard

Reinforcement Learning models benefit from tracking training metrics. FreqAI has integrated Tensorboard to allow users to track training and evaluation performance across all coins and across all retrainings. To start, the user should ensure Tensorboard is installed on their computer:

pip3 install tensorboard

Next, the user can activate Tensorboard with the following command:

cd freqtrade

tensorboard --logdir user_data/models/unique-id

where unique-id is the identifier set in the freqai configuration file.